How To Calculate The Retained Earning For Your Business?

By Sam Nguyen

Drive 20-40% of your revenue with Avada

Retained profits are like a running tally of how much profit the corporation has been able to hang on to since it was created. Any time you deduct any of those earnings in the form of dividend payouts, they go up as the business makes a profit, then down. Retained revenues are something that any company owner would like to see to have a lot of. Retained profits not only mean that a company is sustainable; they also offer an outstanding incentive to compensate owners, produce a new product, and reinvest in the company.

Knowing how to measure sales and income is normal for business owners, but some do not know how to calculate retained earnings. It is also likely that certain company owners do not know what retained earnings are precise. Retained earnings for smaller business groups such as sole proprietorships or single-member LLCs might not even be significant. However, most firms with many owners or holders will need to consider how to measure retained profits, what they are, and the most common ways they can be used.

The formula to answer the question of how to calculate retained earnings and it contributes as a useful tool for the company’s future strategy. However, not every business has the same outcome; you need to understand it properly. This article will walk you through the basic knowledge of retained earnings, the formula for calculating retained earnings, and the comparison between retained earnings and net income.

What exactly are retained earnings?

Before getting to know how to calculate retained earnings, you need to understand retained earnings first.

Retained Earnings Definition

Retained earnings are the total sum of earnings minus the cumulative amount of dividends paid since the company was formed. Retained profits are prior earnings of the company that have not been allocated to its stockholders as dividends.

Retained earnings are an asset?

The sum of a company’s retained earnings is listed as a different line within the balance sheet’s equity portion of the stockholders. However, past profits that have not been paid to stockholders as dividends would usually be reinvested in new revenue-producing reserves or used to decrease the company’s liabilities.

Where do they get retained profits from?

At the end of a financial year, the balances in the revenue, cost, expenditure, and loss accounts of a company are used to compute the year’s net income. These credit balances will also be allocated to the account for retained earnings. The company would have a positive net income because the year’s sales and profits outweigh the costs and expenditures, which allows the surplus to rise in the Retained Earnings report. (If the profits and gains of the corporation for the year are smaller than the costs and liabilities, the result is a net loss that decreases the normal credit balance in the Retained Earnings account.) If the corporation declares a cash payout, the balance in the Retained Earnings account is therefore reduced.

In the Retained Earnings account, what is the usual balance?

A credit balance is a usual balance in the retained earnings account of a successful company. Because revenue accounts have credit balances and cost accounts have debit balances, this is reasonable. This negative amount of retained earnings can be defined as a deficit or cumulative deficit if the balance in the Retained Earnings account has a debit balance.

It is necessary to note that after the payment of dividends, the remaining earnings do not reflect excess income or cash left over. Instead, retained earnings represent what a firm has done for its profits; they are the sum of profit the corporation has reinvested in the company since its inception. Such reinvestments are either sales of properties or changes in liabilities. Once you got why retained earnings matter you will know how to calculate retained earnings correctly.

Examples of retained earnings

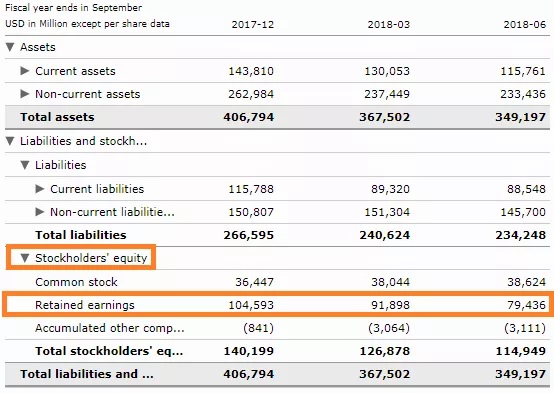

In the balance sheet, corporations officially report retained profits under shareholders’ equity. The statistic has become normal and is listed on the company’s balance sheet as a different line item. For e.g., one of the 2018 balance sheets of Apple Inc. (AAPL) reveals that the firm maintained profits of $79.436 billion as of the quarter of June 2018(Apple. “Q3F2018 Condensed Consolidated Statements of Operations,” Page 2. Accessed July 31, 2020.):

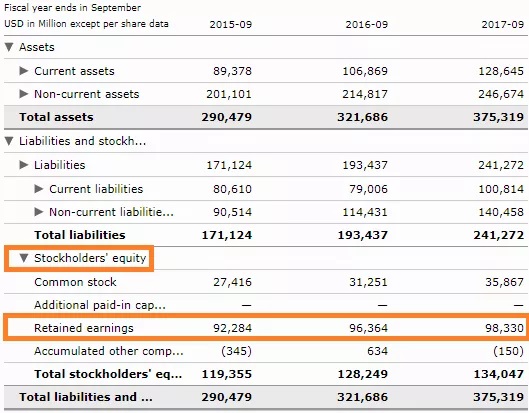

Likewise, as of September 2017, the iPhone manufacturer, whose fiscal year ended in September, had $98.33 billion in retained earnings:

The retained earnings are measured by attaching net earnings to the retained earnings of the previous term (or subtracting net losses from them and then subtracting any net dividend(s) paid to the owners.

The number is measured (quarterly/annually) at the end of each accounting year. As the calculation indicates, residual earnings are based on the previous term’s equivalent figure. Depending on the company’s net profits or loss, the resulting number will either be positive or negative.

Alternatively, it may also contribute to the organization’s negative retained earnings paying high dividends that network exceeds the other estimates. The retained earnings would be affected by any item that influences net income or net loss). These elements include income from purchases, the cost of products produced (COGS), depreciation, and operational expenditures needed.

Apple’s case may illustrate clearly the example of retained earnings and show how to calculate retained earnings. However, it is impossible to look at the definition and cases then figure out the method to calculate the retained earnings for your company. We shall move to the next part of the article to get more information.

How do you calculate retained earnings for your business?

The formula for retained earnings is fairly straightforward:

Present Retained Earnings + Profit/Loss-Dividends = Retained Earnings

When it produces the balance sheet, statement of retained earnings, and other company’s financial statements, the accounting program will do this equation for you.

However, if you happen to measure retained earnings manually, you would need to work out the following three factors before plugging them into the equation mentioned above:

- The last time you measured it, your existing or starting retained earnings, which is just how the retained earnings balance ends up being. (For example, if you build a balance sheet monthly, you can use the retained earnings of last month.)

- Your financial profit/net loss, which will presumably come from this accounting period’s income statement. For example, if you produce certain monthly ones, use the net income or loss of this month. (Here’s how net profits should be calculated).

- You and the other owners vote to take out of the corporation any dividends you distributed during this particular time, which are company earnings. Each shareholder gets a cash payout when you issue a cash dividend. The more an individual holds shares, the higher their share of the dividend is.

To better understand the formula and the notices on how to calculate retained earnings, let’s presume that the company went into operation on January 1, 2020. On January 1, 2020, your retained earnings report will read $0 since you have no earnings to hold.

Then, let’s assume you earn $1,000 in net income (from your declaration of income) in January and don’t question any dividends.

That ensures that the company’s retained earnings on February 1 will be $1,000:

Retained current earnings + Net profits - Dividends = Retained earnings

$0 + $1,000 - $0 = 1,000 dollars

This makes sense: you’ve made $1,000 in gains, and you’ve kept them all.

What are the differences between retained earnings and net income?

Retained profits and net income are linked but different. Since the difference between them, the formula for calculating retained earnings and net income is not the same.

There may be periods where there is a positive net gain for the company but a negative figure in remaining earnings (also called an accrued deficit), or vice versa. Your net revenue is what’s left after you have subtracted operating costs from your profits at the end of the month. Retained earnings are what is left of the net profits after dividends are paid out, and retained earnings are taken into account at the outset.

Have you made $50,000 in profits and $40,000 in expenses? Your net benefit is 10,000 dollars for the month. Nevertheless, suppose you have two owners, and that month you gave $6,000 in dividend payouts to both of them. We can see that we’re left with a negative retained earnings statistic if we go back to our initial equation:

Retained earnings + profit/loss beginning-Dividends= Retained earnings

$0 + $10,000-$12,000 = -$2,000-$2,000

Two ways to get there are net sales and retained earnings, and the two metrics go hand in hand. As the long-term savings plan for your company and net profits serving as an incremental deposit consider retained earnings. For a business, the bottom-line profit received in a given time is net profits. Retained earnings are the distribution over time of those earnings. Such capital may be reinvested in the organization or used as a safety net.

| Net Income | Retained Earnings | |

|---|---|---|

| Basics | Net income is the last measurement of income until you hit the close of a reporting revenue. Next, you calculate the gross profit of the product sold, the sales minus the expense. Then to get to net earnings, you add fixed costs. When you add any irregular sales and deduct any unusual costs from operating earnings, net income is the ultimate product. That is the number of sales that, at the end of the time a corporation maintains. | Retained earnings are often referred to as cumulative earnings because the company retains net sales over time. It is close to a kid putting his allowance in a piggy bank and holding it for whatever he needs versus wasting it. For a couple of factors, businesses usually maintain profits. To invest in new investments, product creation, or marketing, fast-growth businesses maintain profits. A certain level of retained earnings is also preserved by more developed businesses as an emergency fund. Thus, even in a time you have a net loss, it comes out of remaining earnings. |

| Appearance on Income Statement | Their position within financial reporting is a crucial difference between net income and retained earnings. On the financial statement, where all benefit and loss products are included, net income exists. For a particular year, a financial return is quarterly and indicates income received. The top of the net income statement usually reads, “Statement ending March 31, 2018,” or the duration covered by the declaration otherwise denotes. You may either pay net profits to the owners in dividends or reinvest it in the business. |

| Appearance on Balance Sheet | Retained earnings appear on both the balance sheet and the owner’s equity statement. At the close of a given year the balance sheet points out both assets and liabilities. Retained earnings, since it has beneficial value for the company, is an equity account. It is also seen along with the paid-in stock, or the value of ownership stock owned by business investors, on the owner’s equity statement. Fair ownership interest or the company’s net value was paired with retained profits and paid-in stock. |

Conclusion

Knowing the company’s retained profits is relevant because it is a snapshot of the company’s financial health. As the company progresses, it will share a tale about its retained profits. If the account begins to grow, so revenues will grow and the company will remain profitable. That’s a warning that there is a concern that needs to be solved if retained earnings are diminishing.

Potential investors would first look at the retained profits to gauge the health of a company to better assess whether the company is a successful investment. Since people will measure the organization by this amount, knowing what it means is a smart thing for you. We hope that this article will provide you with essential information on calculating retained earnings and further.

New Posts